Market Update There is no doubt that the on-line small business loan marketplace has achieved impressive growth and significant staying power in 2015. There has been much written about the $100 billion+ potential market opportunity born of the banking industry’s multi-year freeze out of the small business borrower. What is noteworthy in the following numbers is the continued rapid conversion of that opportunity into reality. The numbers don’t lie when it comes to the growing loan demand and more importantly, the capital that has formed up to fund this demand and create this emerging asset class. Preliminary 2015 results reflect record growth with $8 billion of originations, up 70% from $4.6 billion in 2014 and four times that of the 2013 origination levels. It is estimated that well over a quarter million individual loan transactions were funded in 2015 with close to half of those transactions coming from repeat borrowers, generally another sign of product satisfaction and market staying power. More significant than the year over year performance is the expectations for continued high growth. Morgan Stanley estimates that the market will expand at a 45% compound annual growth rate through 2020 when on-line small business loan originations are expected to exceed $40 billion for the year.

Clearly, loan growth statistics like these are an indication of active market formation. Other market developments that reflect the health of the still evolving small business loan marketplace include the expansion of differentiated business loan products, the availability of extended loan terms and the gradual implementation of risk adjusted pricing. These developments are further proof of favorable market dynamics driven by large pools of capital entering the market. This money is being directed by discerning and demanding institutional investors like hedge funds and private equity firms and an emerging group of Fintech business leaders seeking both operational scale and the best risk adjusted returns on loans in an increasingly competitive environment.

Competition Benefits Borrowers

This competition is creating an improving environment for both borrowers and the intermediaries that source and deliver borrowers. It’s also putting noteworthy pressure on margins for the lenders and loan investors. This loan price compression is a clear indication of emerging scale allowing the “efficient market theory” of asset pricing to begin to take hold. For those of you who slept through Economics 101, this theory essentially states that the return on an investment (the loan) reflects all relevant information that is available about the intrinsic value of the investment (the loan). Basically, as long as there are opportunities for attractive returns in the small business loan market, new players and more capital will enter, offering lower rates and differentiated terms to secure market share, until a risk – reward equilibrium is found. By all indications, market forces are at work and working.

It is important to remember that the small business loan asset class has not been tested through a significant recession. Thus, the relevant information concerning full credit cycle loan loss rates has not yet entered the calculus on loan pricing. Until loan performance plays out through a downturn it is impossible to fully determine if loan prices are creating sufficient profits to cover future losses and this is likely to contain loan price compression to some degree.

As a leader of a business that works almost exclusively with equipment finance and leasing professionals providing small business loans to their leasing clients, we know many of our customers are overly focused on the loan product’s APR. Viewed narrowly through the APR lens, some believe market forces may not be working fast enough. Frequently perception is every bit as important as reality in emerging markets and our industry continues to have a perception problem on loan pricing. This pricing perception problem must be met with ongoing demonstration that these small business loans, at a practical level, generate favorable borrower economics as currently priced. Borrower acceptance demonstrated through the aforementioned market growth helps with that case. Knowledge of small business lender economics and a continued effort to educate regulators, loan referral sources and potential users of our products on its effective use and the true cost and profitability of this type of credit is also necessary to support market growth.

Practical Application of the Small Business Loan

The decision for a small business to borrow should be and most often is made in light of the ROI on the borrowed funds. For example, let’s say I’m a plumbing contractor in Boulder, CO in business since 2005. I have a 625 FICO (the recession put me upside down on an investment property in 2010 and I exited fully meeting all my obligations but late payments through the process dinged up my credit). I have a real estate developer friend who tells me he is rehabbing a 50 unit garden apartment complex and needs help. He says he needs all the bathrooms fitted with new toilets, sinks and showers and he’d like to give me the job. I do the math and determine that if I can purchase $50,000 worth of inventory, I can win the job with a $110,000 bid and make $30,000 in profit after labor costs and materials. My problem is I don’t have the money to buy the inventory and I need to move fast. An online small business lender will make that $50,000 loan through a streamlined, technology enabled 48 hour underwriting and funding process that requires me to repay $59,500 through an automatically deducted $468.25 payment per business day over the term of the 6 month project. By securing that loan at a dollar cost of $9,500, I’m able to lock up and complete the job creating $30,000 of income for my employees and subcontractors and a $20,500 profit for my company. This loan is clearly an effective way to advance my small business’s objectives. However, this loan also has an APR over 70% and potentially violates usury laws in over 20% of the United States including my theoretical home state of CO.

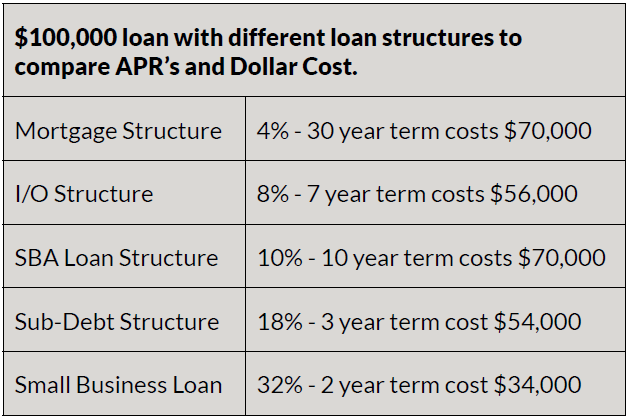

Through this example, it’s clear why this market is growing. Even when APR’s are high, the dollar cost of the credit has utility for the borrower. Given the choice of passing on the job or quickly borrowing $50,000, repaying $59,500 and capturing the $20,500 profit, even if the borrower’s state regulators object to the loan, the borrower’s choice is obvious. APR’s Can’t and Don’t Tell the Whole Story Unfortunately, there is a tendency by many to make rate comparisons to other asset classes thereby clouding one’s analysis of the small business loan. Comparing just APR’s and ignoring dollar costs for an online un-restricted working capital loan relative to longer term, secured, seasoned asset classes like mortgages, leases or senior secured loans is a misguided exercise. Following are several examples of loan structures with both APR’s and total borrowing costs that make the point:

Evaluating the utility of the loan for the borrower and the attractiveness of making the loan for the lender means assessing the actual dollars of cost for the borrower and dollars of revenue to the lender. Typical small business borrowing needs are generally not well served by Bank provided business loans which, though infrequently available, are characterized by larger loan sizes, longer durations, rigid collateral, financial statement and credit profile requirements and a lengthy due diligence and decision making process. Basically the longer the debt is outstanding the more revenue the Bank generates even with relatively low APR’s, as in the SBA and mortgage examples above.

By contrast, and as in my Boulder, CO plumbing contractor example, small businesses often seek low dollar loans where ROI is captured based on quick funding and disciplined repayment that keep the dollar cost of the credit down. Ironically driving down the dollar cost of the credit by paying it off more quickly is exactly what drives up APR’s. For both borrower and lender, it is the actual dollars, not APR’s, that drive the economics in this market.

The Importance of Lender Profit for Small Business Loan Availability

Large pools of capital will not continue to be available for funding small business loan transactions without a market that delivers a proper rate of return on originated loans. Lender performance is another means of assessing the state of the market. Interestingly, the largest player in the small business online lending industry, OnDeck is public and as such makes available financial and operating data. As the largest player in the market with a loan portfolio that has a weighted average APR of 42%, one would assume the company is a highly profitable business. Surprisingly, OnDeck has only recently achieved profitability with a 5% pre-tax margin in the most recent quarter after 8 years in business.

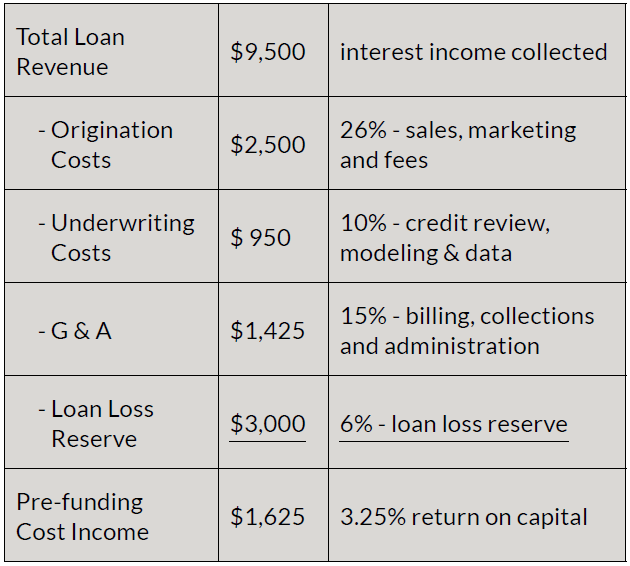

Breaking down unit level economics helps explain why it is necessary to price loans as the industry does. Using the Boulder, CO contractor’s 70%+ APR loan as an example can shed some light on the unit level economics and narrow margins for the lender on a typical small business loan:

Reasons for Optimism

A conclusion one might reach from this article is that small business loans are expensive for borrowers and the economics for the lender barely justify making the loan. A somewhat bleak conclusion. Another way to look at it is to recognize that with the inevitable expanded scale that comes from unmet demand, the economics of the small business working capital lending business will get better and through competition, that will translate into better price, terms and product choices for borrowers, further expanding the market.

Strong market forces are at play here on both the demand and supply side and given space and time to continue to develop, the primary engine for US economic growth, the small business, will benefit from continued expanded access to capital.

Article Supplied by Channel Partners Capital ![]()